The European Energy Market - Liberalization & Unbundling

Definition

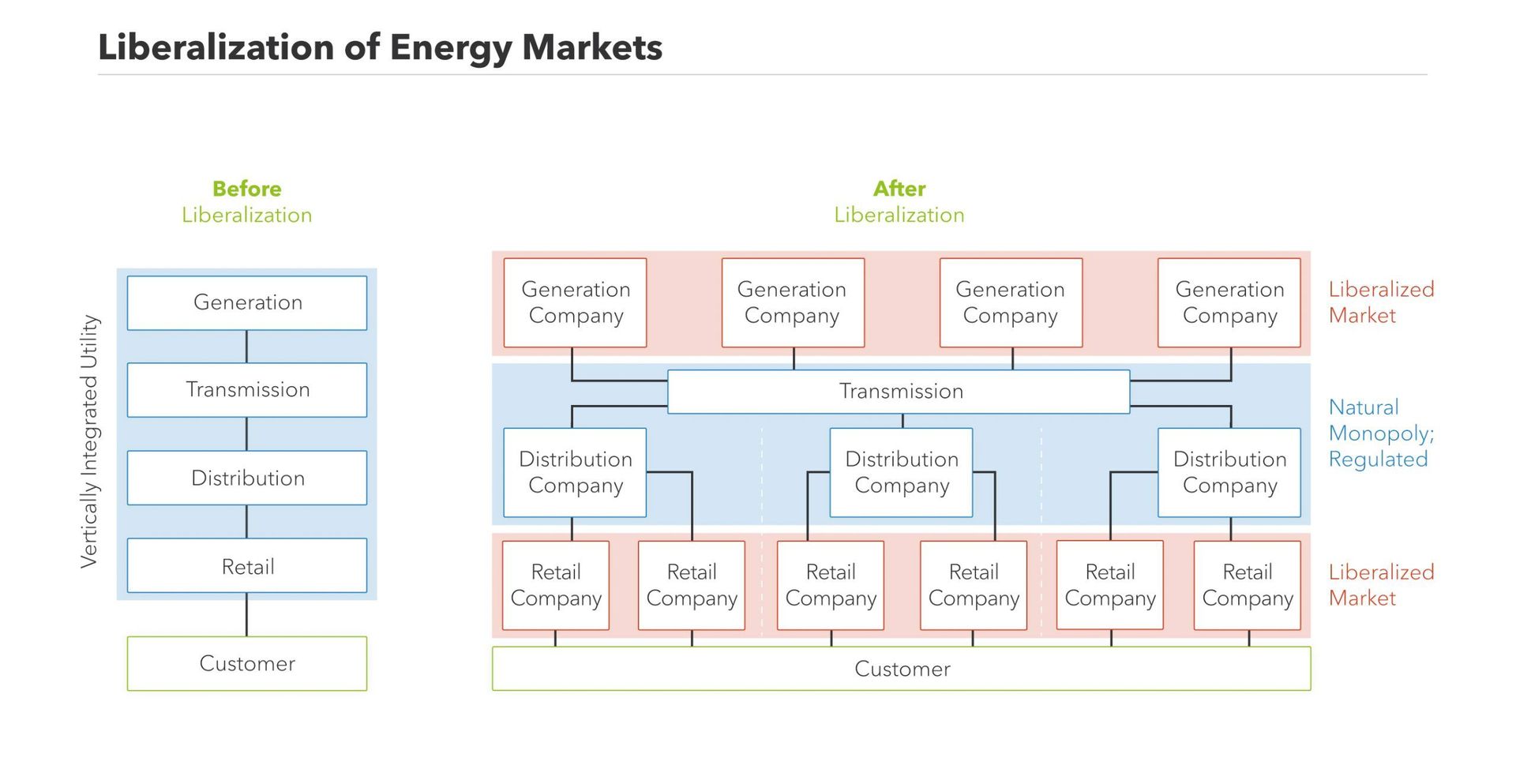

Electricity travels a long way from the place where it is generated to where it is consumed. In the current European electricity system, the different stages of in power provision are split up. There are the generation companies who take care of the production of electricity in their power plants. The electricity is transmitted via the high-voltage grid, often referred to as the transmission grid. It is operated by the transmission grid operator (TSO). The suppliers (or retailers) take care of the actual provision of electricity to the end consumer. They buy electricity at the wholesale market and it is transported to the customer through the distribution grid to which households and companies are connected. This part of the system is characterized by lower voltage levels and is operated by the distribution grid operators (DSOs). You can learn more about the function of the different players in the electricity grid in this article.

In an ideal setting, both production and supply are fully competitive activities. It means that none of the companies in the generation sector can influence electricity prices on the wholesale market by using their market power. This should eventually lead to lower prices for the consumer. Also in the retail market, where the suppliers sell electricity contracts to the end-user, free competition is in the benefit of the consumer. Households now have the choice to pick the supplier that offers them the best tariff and service.

In reality, a perfect competition seldomly exists. Especially in industries with large capital investments and large infrastructure, the activities are typically in the hands of a few large companies. The regulating instances who monitor abuse of market power quantify the level of free competition with the so-called concentration ratio CR3. An analysis by ACER, the Agency for the Cooperation of Energy Regulators in Europe, revealed that the level of market concentration is still quite high in Belgium. We perform worse than our neighbor Germany, but better than France.

Transmission and distribution grid are central assets

The transmission and distribution grids connect generation and consumption. For this job, extensive infrastructure is required. The transmission grid, often called the high-voltage grid, transmits the power over long distances. In substations around Europe, the power is brought to a lower voltage level in transformer substations. From there on the electricity is further distributed over the distribution grid towards the end-consumers. Very large industrial consumers are often connected directly to the transmission grid, though.

The transmission and distribution grids are central assets. It is almost impossible for another company to erect a second grid. It requires massive investments, but also the permits for building such a large infrastructure. Therefore, energy infrastructure is de facto a natural monopoly.

To avoid market power abuse and assure a reliable operation of the grid, not only the ownership is unbundled but the natural monopoly is also regulated. An independent regulator guards the level-playing field of the free market. For example, they monitor the access tariffs the TSOs and DSOs charge to producers who want to connect their plant to the electricity grid. In the end, there can only be free competition between generators when there is non-discriminatory access to the power grid.

In Belgium, the transmission grid operator (TSO) is Elia. The distribution grid is split up in several geographical areas. Some examples of Belgian distribution grid operators (DSO) are Eandis and Infrax (Sibelga (Brussels), ORES and RESA (Wallonia).The CREG is the national regulator for both electricity and gas markets. They guarantee transparency and competitiveness of the energy market, defend consumers’ interest and advice authorities on energy issues.

From a monopoly to a single European electricity market

In fact the European electricity market with free competition as we know it today is very young and still in development. Three decades ago, the European electricity sector was a monopoly. Vertically integrated companies were responsible for the generation, transmission, distribution, and supply of electricity to the consumers. These companies virtually set the electricity prices without much competition to challenge them. Since those companies also held the grid infrastructure, market access of new players was impossible.

In 1996, the European Union started to gradually open the market for competition – to liberalize the energy market just like it did before with several other sectors. The aim was and is to create one single integrated internal European electricity market across all EU member states to reduce overall grid costs and benefit security of supply.

More information

A key step in this process was and is the unbundling of the European power sector with the aim to split up the generation, transmission, distribution and delivery activities. The vertically integrated companies could no longer both generate, trade and supply electricity while managing the transmission and distribution networks. This unbundling didn’t happen overnight. In the first energy package in 1996, only accounting unbundling was required. It demanded the vertically integrated companies to split up the bookkeeping according to the different activities. This was clearly not sufficient to create a competitive market. In the second directive, introduced in 2003, legal unbundling was demanded. It meant that a single company was allowed to operate in only one of the activities of the electricity value chain: either production, transmission, distribution or supply. It also demanded that by 2007 all European customers should have the ability to choose their supplier. But because the different companies still could be part of the same holding, the owners of those companies still had quite some market power. In the third energy package the next step towards free competition was made by introducing ownership unbundling.

Read more about the different energy markets...

Disclaimer: Next Kraftwerke does not take any responsibility for the completeness, accuracy and actuality of the information provided. This article is for information purposes only and does not replace individual legal advice.